The Modi government replaced the earlier crop insurance schemes with the Pradhan Mantri Fasal Bima Yojana (PMFBY) in February 2016 claiming that the new scheme would be instrumental in ending farmers’ woes. Three years later, it is time to assess how far farmers’ interests have been advanced by this scheme.

The Modi government replaced the earlier crop insurance schemes with the Pradhan Mantri Fasal Bima Yojana (PMFBY) in February 2016 claiming that the new scheme would be instrumental in ending farmers’ woes. Three years later, it is time to assess how far farmers’ interests have been advanced by this scheme.

The Modi government replaced the earlier crop insurance schemes with the Pradhan Mantri Fasal Bima Yojana (PMFBY) in February 2016 claiming that the new scheme would be instrumental in ending farmers’ woes. Three years later, it is time to assess how far farmers’ interests have been advanced by this scheme.

What insurance coverage shows about farmer’s perception of the PMFBY

Farmers taking crop loans are compelled to take crop insurance. Crop loans are given almost entirely by public sector financial institutions and cooperative banks which, following government directives, automatically deduct insurance premium from the loans they make to the farmer.

By compelling farmers to take insurance, the government first of all ensures a minimum number of captive customers to make crop insurance viable. Second, the insurance serves as collateral for the farmer’s loan, since any insurance payout in the event of crop loss is routed through the same financial institution.

The government labels farmers whose insurance premium is deducted compulsorily from a crop loan as ‘loanee’ farmers and all others as ‘non-loanee’ farmers. A rise in the number of crop loans can result in a rise of ‘loanee’ farmers. ‘Non-loanee’ farmers are presumed to have taken crop insurance voluntarily and a rise in their numbers would be a sign that farmers perceive insurance to be beneficial.

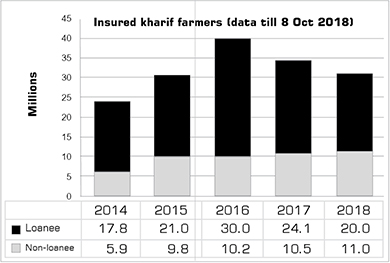

Sharp fall in enrolment of farmers

|

The chart shows the number of farmers who have taken crop insurance during the kharif (monsoon) season over the last several years. The kharif season accounts for roughly two third of the insured farmers and crop area. (The data up to 2016 has been retrieved from the 2017 CAG report on crop insurance and for later years from Lok Sabha and RTI answers.)

Enrolment was highest in 2016, the first year of the implementation of the PMFBY. Three-forth of the farmers enrolled that year were ‘loanee’ farmers whose insurance premium contributions would have been forcibly deducted from their loan accounts. After that, enrolment sharply fell in the next two years. The PMFBY did not have any impact on the ‘non-loanee’ enrolment which remained at the same level as it was in 2015.

Government’s excuses for the fall

The government has advanced several reasons to explain the lower number of insurance policies linked to loans, that is, the lower number of ‘loanee’ farmers.

One is that when states announce farm loan waivers, farmers keep payments on old loans pending, making them ineligible for new loans. This would mean a lesser number of farmers applying for new crop loans. A second reason is that the introduction of Aadhar in the loan approval process has eliminated the earlier practice of some farmers taking multiple loans for the same crop.

But an analysis of kharif data shows the number of insured farmers came down by a large percentage not only in Maharashtra and UP which announced farm loan waivers during the relevant period, but in seven other states – Bihar, Chattisgarh, Gujarat, Haryana, MP, Rajasthan and West Bengal. These nine states account for more than 80% of the farmers insured for kharif 2016.

Further, in all these states, the ‘non-loanee’ numbers either remained almost unchanged or saw a fall. Why is it that the farmers who did not get loan-linked insurance in these states (as they did not take loans) not voluntarily opt for insurance if this was to their benefit?

What are the real reasons for farmers opting out?

What is absolutely clear is that a large number of farmers avoided taking crop insurance under the new scheme unless compelled.

Farmers have faced many problems with crop insurance. These include: not even knowing that they have insurance (as premium deduction is made without their consent); underestimation of crop loss by the government; rejection of claims by insurance companies on various pretexts; lack of avenues for redressal of their grievances; and above all, delays in claims settlement.

It is imperative for farmers that claims of crop loss for any season are settled before the start of the next season, as they need the money to commence sowing. There are huge delays with farmers having to wait up to 18 months. Farmers have been forced to take collective action, including opposing mandatory deduction of insurance premium from their crop loan accounts.

What the usage of public funds under PMFBY reveals about government’s priorities

Just as any other insurance, crop loss insurance works on the idea of spreading risk across a large number of people exposed to the same risk – in this case, farmers.

Insurers consider the risk of crop damage in India to be high as there is a record of a significant loss of food grain production once in every three years. Therefore the premiums arrived at on actuarial considerations that is, after a statistical analysis of past production figures, are high. Such high premiums are unaffordable for small and marginal farmers who constitute 86% of the farmer population.

Public funding models of crop insurance

Two models for public funding of crop insurance have been tried in India. Before the launch of PMFBY, multiple insurance schemes were in operation using both these models.

In a trust model, farmers pay premiums to a trust which manages the funds and compensation payouts. Premiums are set at levels affordable to farmers. When crop loss compensation claims exceed the capacity of the trust to pay, the state steps in and makes up the deficit.

This model was followed by the National Agricultural Insurance Scheme (NAIS). Premiums were fixed by the government at relatively low levels – averaging less than 3.5% for kharif crops as a whole. A public sector entity, the Agriculture Insurance Company (AIC), acted like a trust and collected premiums and serviced claims. If claims exceeded the ability of AIC to pay, the government with central and state contributions made good the deficit.

In the insurance model, an insurance company collects premiums and pays compensation. Premiums are fixed in such a way as to minimise the risk borne by the company and allow it to cover its overheads and make a profit. Farmers pay a portion of the premium and the state pays the rest. In this way, the government together with the farmers actually absorb most of the risk.

This model was used in two schemes – the Modified National Agricultural Insurance Scheme (MNAIS) and the Weather Based Crop Insurance Scheme (WBCIS). Premiums and claims were managed by insurance companies. Insurers charged premiums averaging 10-11% across India for kharif crops, which were paid partly by farmers and partly by the government with central and state contributions. In order to control its overall expenditure, the government set caps for the premium subsidy and premium rate.

The UPA government was keen to replace the trust model with the insurance model schemes (which it initiated) but could not succeed entirely because of opposition from state governments. In 2015-16, the scheme based on the trust model, the NAIS, accounted for 64% of the insured farmers and 70% of the sum assured. The other schemes based on the insurance model not only had a smaller footprint, but most of the farmers enrolled in them had been compelled to take insurance along with public sector loans. Voluntary participation was virtually non-existent in the MNAIS and less than 3% of the farmers enrolled in the WBCIS.

The Modi government carried out at one shot what the UPA had been struggling with. All three UPA era schemes were replaced by the PMFBY in 2016. The PMFBY conformed to the insurance model with higher all India average premiums of 12-15% for kharif crops. The government fixed the premium contribution to be paid by farmers at levels similar to the NAIS and paid the rest with central and state contributions.

From the insurer’s perspective, the PMFBY was made much more attractive than earlier schemes. The caps set by government earlier on the sum insured as well as the ‘premium subsidy’ provided by the government were relaxed. This meant that insurers could look forward to a potentially larger business from higher sums assured as well as higher enrolment. Since premium paid by farmers was fixed at low levels, the government would be largely footing the bill.

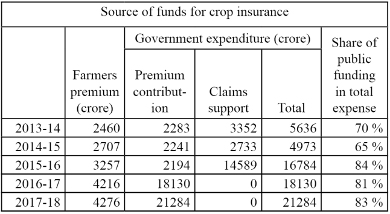

The sources and usage of funds for crop insurance

|

The funds earmarked for crop insurance have increased dramatically over time. The state has been the major contributor, providing over 80% of the funding in the last three years (See attached table which presents data gathered from answers in Parliament).

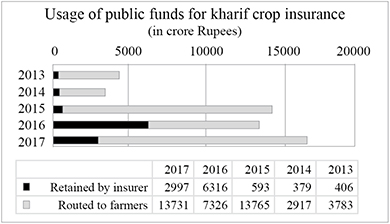

How much of the money spent by the government reaches the farmers?

|

The chart here indicates the portion of government expenditure retained by insurers after settling claims of farmers during successive kharif seasons. Data has been gathered from government publications and answers in Parliament. The portion shown as ‘routed to farmers’ is the flow of money to farmers over and above the premium amount collected from them.

Before 2016, insurers retained less than 12% of government funding for any season and the rest reached farmers. That situation changed dramatically with the advent of the PMFBY.

Examining 2015, the year before PMFBY was implemented, is instructive. This was a major drought year. The bulk of claim payouts to farmers was under the NAIS, which accounted for 70% of the sum assured, where the government paid the major share of the claims as they exceeded AIC’s capacity to pay. This meant that almost all the money ploughed in by the government was paid to farmers.

With the advent of the PMFBY, upwards of 80% of the premium is paid by the government to the insurers who have retained about 46% and 18% of it respectively in the last two kharif seasons. The amount retained by insurers has increased by nearly ten times after the PMFBY was introduced in 2016. Over two kharif seasons, 2016 and 2017, insurers retained Rs 9,300 crores!

Is the insurance model superior to the trust model?

Answering to criticism that the Modi government has allowed insurers to make windfall gains, the agriculture secretary has recently claimed that the PMFBY insurance model is superior to the NAIS trust model as the government no longer carries the liability for claims which were “unlimited” earlier and could result in a huge payout in case of a major drought (Times of India, Dec 3, 2018).

The fact is that private insurance companies always try to minimize the risk they carry. They ensure that risk is borne by the insured, in this case farmers – and the government which pays over 80% of the premium. High risk means high premiums.

It can be that in some specific year a situation arises when the payout to farmers is higher than the premium collected. However, when cumulated over several years, premium collected must exceed the payouts to farmers and overheads to enable insurers to turn in profits. Thus the government will spend more money over several years on premiums than if it just provided claims support when needed as in the NAIS.

Who benefits from the PMFBY?

The PMFBY allows the participation of private insurers by allowing them to set premiums. The usual argument in favour of private service providers is that because of competition they are more responsive to customers. This is not valid for the PMFBY as there is only one insurance provider in any area and the farmer has no choice. The government has to cajole or threaten insurers for something as basic as timely settlement of claims.

The entire infrastructure used for insurance in rural India belongs to the public sector – from rural bank branches offering insurance and collecting premium to state machinery to determine crop yields and measure crop loss. Reports suggest that private insurance providers have hardly any “boots on the ground” and farmers find it difficult to access these insurers for grievance redressal. The insurance companies do not add any value as intermediaries between the government and the farmers.

The government currently pays 80% – 85% of the premium for crop insurance. The quantum of public expenditure is large with close to Rs 40,000 crore spent in the two years 2016-17 and 2017-18.

Under these conditions how is it justifiable for the government to work through insurance intermediaries and pay for their overheads and profits? It appears that the main consideration of the Modi government when it designed the PMFBY was providing business to corporate insurers rather than providing relief to stricken farmers.